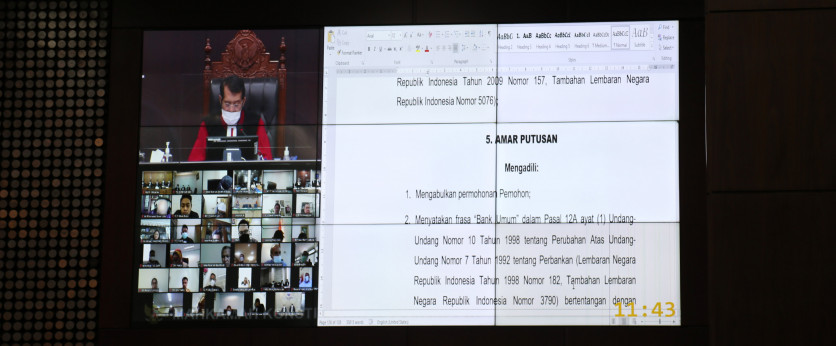

Chief Justice Anwar Usman reading out the verdict of the material judicial review hearing of Article 12A paragraph (1) of Law No. 10 of 1998 on Banking, Wednesday (9/29/2021). Photo by Humas MK/Bayu.

Wednesday, September 29, 2021 | 17:38 WIB

JAKARTA, Public Relations—The Constitutional Court (MK) granted the material judicial review petition of Law No. 10 of 1998 on the Amendment to Law No. 7 of 1992 on Banking. The Decision No. 102/PUU-XVIII/2020 was pronounced on Wednesday, September 29, 2021 in the plenary courtroom.

“[The Court] adjudicated, grants the Petitioner’s petition; declares the phrase ‘Commercial Banks’ in Article 12A paragraph (1) of Law No. 10 of 1998 on the Amendment to Law No. 7 of 1992 on Banking in conflict with the 1945 Constitution of the Republic of Indonesia and null and void insofar as not interpreted as ‘Commercial Banks and BPR,’” said Chief Justice Anwar Usman reading out the verdict.

As such, he added, 12A paragraph (1) of the Banking Law, which initially read, “A Commercial Bank may purchase Collateral, whether in whole or in part, either through auction or outside auction according to willful submission by the owner of the Collateral or according to power of attorney by the owner of the collateral to sale outside auction in the event that a Debtor Customer fail to meet its obligations to the Bank, provided that the purchased Collateral shall be chased in at the earliest opportunity,” now reads, “A Commercial Bank and a BPR may purchase Collateral, whether in whole or in part, either through auction or outside auction according to willful submission by the owner of the Collateral or according to power of attorney by the owner of the collateral to sale outside auction in the event that a Debtor Customer fail to meet its obligations to the Bank, provided that the purchased Collateral shall be chased in at the earliest opportunity.”

Also read: Provision Restricting Collateral Purchase by Banks Challenged

Executive director of PT Bank Perkreditan Rakyat (BPR) Lestari Bali, Pribadi Budiono, filed the petition to challenge Article 12A paragraph (1) of the Banking Law, alleging that the provision allows only commercial banks to take over the collateral of bad credit customers. He claimed to have suffered loss due to the enactment of the phrase “Commercial Banks” in the Banking Law, as it allows only commercial banks to take over the collaterals of customers with nonperforming loans through auctions. Meanwhile, BPRs do not have this right. Therefore, the Petitioner feels he has received discriminatory treatment and injustice in obtaining equal opportunity and benefits for equality and justice that commercial banks receive in taking over its customers’ collaterals of through auction to settle their nonperforming loans.

Also read: House: BPR Can Buy Customers’ Collaterals Through Auctions

Like Commercial Banks

In the legal considerations read out by Constitutional Justice Enny Nurbaningsih, the Court holds that microcredit banks (BPRs) provide the same financial services to the community as commercial banks, sharia commercial banks, and sharia BPRs. Although commercial banks have more business types than BPRs, some business types that BPRs run are similar to those that commercial banks do, such as collecting funding from the community in the form of savings, offering credit loans, and providing financing for its customers. In addition, Article 15 of Law No. 7 of 1992 firmly states that the provisions in Article 8 and Article 11 of Law No. 7 of 1992 and Law No. 10 of 1998, which are part of the regulations on commercial banks, also apply to BPRs’ businesses.

Basically, what distinguishes the types of business by commercial banks from those of BPRs, Justice Enny added, is that commercial banks can run payment traffic services, but in relation to the issues in the a quo petition, both commercial banks and BPRs can run a lending business.

“Moreover, the provision of Article 8 paragraph (1) of Law No. 10 of 1998 strictly states, ‘In extending Credits or Financing based on Sharia Principles, a Commercial Bank shall have confidence based on thorough analysis on the intention, capability, and ability of a Debtor Customer to repay their debt or financing according to the agreed terms,” she said.

Also read: Bank Indonesia: AYDA, Solution for Nonperforming Loans

Difficulty Developing

Because the provision also applies to BPRs based on Article 15 of Law No. 7 of 1992, Justice Enny added, in providing credit or loans to their customers, BPRs also have the same obligation as commercial banks to carry out in-depth analysis of prospective debtor customers. The problem is that, despite an analysis on the debtor customers’ intention, capability, and ability to repay the loan, in reality, they could be unable to do so, causing nonperforming loans. This is more likely during economic decline.

If such a condition is ignored, the Court states, it is highly likely that most or all BPRs will have difficulty developing and may even need to close their business. In contrast to BPRs, to deal with such a condition, commercial banks and sharia BPRs, can use the AYDA instrument to resolve nonperforming loans, because this is clearly stipulated in the law. In contrast, BPRs, which are regulated in the Banking Laws No. 7 of 1992 and No. 10 of 1998, cannot implement AYDA either through auctions or outside of auctions when the mechanism, both through auctions and outside of auctions, is an effort to resolve the nonperforming loans by accelerating the settlement of debts or loans.

“This is given that the resolution of nonperforming loans will affect the financial soundness and liquidity of the bank. Moreover, Laws No. 7 of 1992 and No. 10 of 1998 stipulates that loans are one form of business that BPRs can carry out, so BPRs should be given the ease of settling nonperforming loans,” Justice Enny read out.

AYDA and loans, she said, are interrelated and inseparable, as applies to commercial banks, sharia commercial banks, and sharia BPRs. It is part of the precautions common in financial services.

Also read: Expert: Collateral Takeover, BPR’s Main Instrument Against Nonperforming Loans

BPRs Guaranteed by Law

The Court maintains that the BPR is a banking institution that is guaranteed by the law. It has developed since 1998 when Law No. 7 of 1992 has not been amended.

BPRs, Justice Enny said, has an important role in growing the national economy, including among people in remote areas that commercial banks might not reach. Therefore, the same opportunities as commercial banks to maintain their businesses should be availed to them. Moreover, Article 40 paragraph (1) of Law No. 21 of 2008 accommodates sharia BPRs, whose business markets are similar to those of conventional BPRs, to join auctions of collateral. If the AYDA instrument and mechanism through auction can be implemented to BPRs, it would facilitate them in resolving nonperforming loans.

Also read: BPR Not Prohibited from Taking Over Collateral Through Auction

Different Interpretations

Justice Enny further explained that regulators and national banking authorities have made efforts to accommodate BPRs so it can purchase entire or part of collateral through or outside of auction, by issuing the Financial Services Authority Regulation (POJK) No. 33/POJK.03/2018 on December 27, 2018, after Bank Indonesia had issued the BI Regulation (PBI) No. 13/26/PBI/2011 on the Amendment to PBI No. 8/19/PBI/2006 Earning Assets Quality and Establishment of Provisions for BPR’s Earning Assets, each of which stipulates that AYDA is an asset obtained by BPRs to settle credits, either through or outside of auction, based on voluntary submission by the collateral owner or based on a power of attorney to sell outside the auction by the collateral owner, in the event that the debtor is declared to have defaulted.

However, the Directorate General of State Assets Management (DJKN) also issued the Letter No. S-407/KN.7/2012 on April 12, 2012 addressed to heads of DJKN regional offices and heads of State Assets and Auction Services (KPKNL) all across Indonesia, which used Article 12A paragraph (1) of Law No. 10 of 1998 to determine that only commercial banks may purchase entire or part of collateral through or outside of auction.

As such, Justice Enny said, different interpretations of Article 12A paragraph (1) of Law No. 10 of 1998 exist, which will have impacts on the auction of collateral nationally and discriminate against BPRs in collateral auctions. This will also lead to legal uncertainty and eliminate equal opportunity for the Petitioner and BPRs in joining auctions of their nonperforming debtor customers’ collateral.

After the Court considered the Petitioner’s petition, Justice Enny added, it decided that legal certainty is required for Article 12A paragraph (1) of Law No. 10 of 1998 to avoid multiple interpretations and to provide equal treatment in relation to action to all BPRs in all regions nationally, as well as to provide equal treatment for conventional and sharia BPRs. Therefore, the Court stressed that the phrase “Commercial Banks” in Article 12A paragraph (1) of Law No. 10 of 1998 must be interpreted as “Commercial Banks and BPRs.”

The provision on BPRs should be put in Chapter III Part III of Law No. 7 of 1992 as it concerns the regulations of banking businesses. Meanwhile, the Petitioner did not request the judicial review of any other article and the Court did not find any other article related to collateral purchase through and outside of auction by BPRs in Chapter III Part II of Law No. 7 of 1992.

The Court understands that its interpretation of Article 12A paragraph (1) of Law No. 10 of 1998 seems as if it could change banking business arrangements as stipulated in Law No. 7 of 1992. However, business arrangements for commercial banks and BPRs are not absolutely separate and are even related because Article 15 of Law No. 7 of 1992 provides a firm legal basis for imposing the same obligations that apply to commercial banks, including the terms and conditions for granting credits.

Nevertheless, the Petitioner did not request the judicial review of Article 15 of the a quo Law. Therefore, for legal certainty, fair treatment, and benefits for BPRs and debtor customers, as well as in consideration of the constitutional loss that the Petitioner experience, as stipulated in Article 28D paragraph (1) and Article 28H paragraph (2) of the 1945 Constitution, there was no other option for the Court but to interpret Article 12A paragraph (1) of Law No. 10 of 1998. “Therefore, the Court is of the opinion that the Petitioner’s argument is legally valid,” Justice Enny stressed.

Writer : Utami Argawati

Editor : Lulu Anjarsari P.

PR : Andhini S. F.

Translator : Yuniar Widiastuti (NL)

Translation uploaded on 10/1/2021 09:36 WIB

Disclaimer: The original version of the news is in Indonesian. In case of any differences between the English and the Indonesian versions, the Indonesian version will prevail.

Wednesday, September 29, 2021 | 17:38 WIB 335